Tax invoices

The following are general guidelines for tax invoices in Vietnam:

Creation of invoices:

- A business may adopt different forms of invoice such as self-printed invoice, print-to-order invoice, electronic invoice;

- Invoices must not carry identical serial numbers;

- Invoices must be printed on quality paper and ink, which can last as long as the period of archival of documents, as required by the Accounting Law (ie. 10 years);

- For self-printed invoices generated by IT equipment:

- Serial numbers must be automatically generated;

- Each slip of the invoice must be printed only once; if more than once print is require it must indicate “copy”

- The software must have access control to prevent unauthorized alternation of data

All compulsory information below must be in the same page:

- Prescribed name of invoice e.g. VAT Invoice or Sales Invoice

- An additional name is option but it must be stated after the prescribed name, in smaller font and in parenthesis e.g. VAT invoice (Warranty), or VAT Invoice (Receipt), Export Invoice (Commercial Invoice)

- Serial number (including alphabet, year of issue and a 7-digit number)

- Name of copy e.g. File Copy, Customer’s Copy, the 3rd copy may be customised

- Name, address and tax ID of the seller and the buyer

- Designation of goods/services, unit, quantity, unit price, totals in both figures and words

- For a VAT invoice: prices before VAT, VAT rate, VAT

- Signature blocks for both the seller and buyer who must sign, date and state their full name. In addition, seller must affix a stamp (if any).

- Name and tax ID of the invoice printer

Optional information in a tax invoice:

- Logo, decorative layout or advertisements;

- The font of optional wordings must be smaller than the smallest font of the compulsory wordings;

- The optional info must comply with relevant laws and must not overlap the compulsory info;

Language requirements:

- The default language is Vietnamese

- Where a second language is used:

- it must be written to the right in parenthesis (); or

- below the Vietnamese information and in smaller font

- All numbers must be numerical numbers

- All digits must be in the same size

- Decimal mark must be a coma “,”

- The thousands’ separator must be point “.”

- However, multi-national companies with global IT sales system may interchange the use of “,” and “.” in their numerical info and use Vietnamese without ascent but they must ensure that will not mislead readers and they must register with the local tax office.

Rules for invoice issuance:

- Before putting the invoices (other than invoices acquired from tax office) to use, business must notify the local tax office (using Form 3.5);

- If the business is relocated, a similar notice must be lodged with the tax office in the new location.

- These notice must be lodged at least 5 days before the invoices are put to use and within 10 days following the date of such notice.

- A copy of this notice and sample invoice must be displayed at the business premise throughout the period of usage.

- Where a business and its branches use the same invoice from, the branches must notify the respective local tax office.

- Local tax offices are required to notify the taxpayers within 2 working days if a notice does not meet the requirements.

Rules for use of invoices:

- Only registered invoices may be issued to buyers;

- Sellers must issue invoices in all sales transactions, including all cases of promotional, advertising or sample merchandises, free products, exchange of products, products in lieu of salary or for internal consumption, loan or return of inventories (other than inventories issued for internal movement);

- Details on the invoice must be accurate; no alternations; no omissions; the same type of ink color; no red color; numbers must not be spaced; no writing on the pre-printed wordings; unused spaces must be crossed out.

- More than one copy of invoice may be made, but details in all copies must be consistent.

- Invoices must be issued in ascending order of serial numbers

Canceling/Adjusting an invoice:

- If an erroneous invoice has not been given to the buyer => all copies must be canceled, crossed out and retained;

- If the invoice has been given to the buyer but goods/services have not been delivered and both seller and buyer have not reported it for taxes => the buyer must withdraw the invoice, cancel it, and issue a new invoice;

- If the goods/and services have been delivered and the invoice has been reported for taxes => the buyer must issue an adjusting invoice and adjust all relevant tax returns. An adjusting invoice must not carry a negative (-) amount. Instead, it must specify whether it is an increasing adjustment or decreasing adjustment.

Reporting lost/damaged invoices:

- All cases of loss/damage of invoices must be reported to the tax office within 5 days following the incidence;

- Where Copy 2 of an issued invoice is lost/damaged, the seller and the buyer must enter into a Minutes to document the incidence.

- The buyer then may use a photocopy of Copy 1 certified by the seller for tax purposes.

Reporting invoice usage:

- Every quarter, businesses are required to report to the tax office the level of their invoice usage.

- A report of invoice usage (Form 3.3) must be lodged together with the VAT return of the 1st month following the reporting quarter;

- Businesses undergone M&A, consolidation, liquidation, insolvency, change of ownership must also submit this report together with their final tax return.

- Businesses relocating to a new location must report to the tax office in the place of origin (using Form3.10), before notifying the tax office in the new location of their new invoice format.

Penalties for invoice related offences:

- A maximum penalty of VND100 million and 3-year ban apply to offences related to self-print, e-invoices, print-to-order invoices.

- Some other maximum penalties:

- VND20 million for failure to comply with notification requirements;

- VND5 million for failure to provide a customer with invoice;

- VND20 million for failure to issue an invoice (except for sales below the threshold of VND0.2 million);

- VND25 million for discrepancies between copies of an invoice or failure to report lost invoices;

- VND60 million for misuse of invoice;

- VND75 million for give-away or sale of blank invoice;

- VND100 million for issuing fictitious invoice;

- etc.

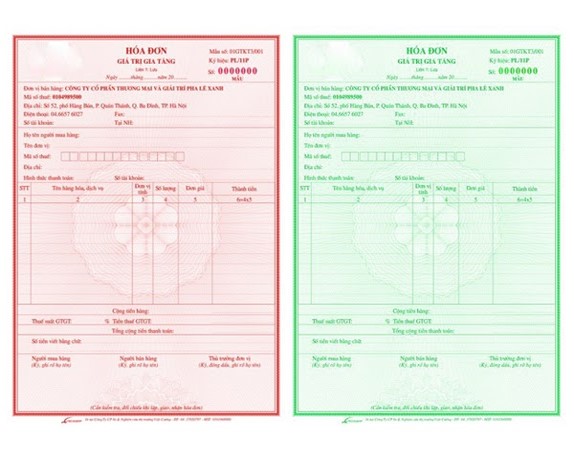

Below is what a standard tax invoice looks like: